ISBN: 978-1-63369-178-0

My rating: 85/100

See Book Notes for other books I have read. If you like my notes, go buy it!

By Clayton M. Christensen

Tagline: When new technologies cause great firms to fail.

Key Points:

- “Good” management principles (like listening to customers and investment in higher margin products) were precisely the reason large firms lost to up and coming businesses with disruptive technologies.

- Fortune favors the bold and the brave. Creating new markets is significantly less risky and more rewarding than entering established markets against entrenched competition. Firms that sought growth by entering small, emerging markets logged twenty times the revenues of the firms pursuing growth in larger markets.

- Value Network – the context within which a firm identifies and responds to customers’ needs, solves problems, procures input, reacts to competitors, and strives for profit. Note that value networks can shift over time.

- Disruptive technologies need to be sold to anyone that will buy.

- Establish independent organizations to pursue disruptive technologies. They are more flexible at adapting to the emerging market needs and can get excited about small orders.

- Match the size of the organization to the size of the market.

- Markets that do not exist cannot be analyzed.

- The values of an organization are the criteria by which decisions about priorities are made.

- Four phases of buying hierarchy: functionality, reliability, convenience, and price.

I was a little confused about the seeming contradiction in statements made regarding the risks and rewards associated with disruptive technologies. On one hand, Clayton seems to say that everyone everywhere should be investing in disruptive tech because it will yield far greater returns than those investments made in sustaining technologies, however, he also states the risks of investing in disruptive tech are so much higher. Obviously there is a break point somewhere, a tipping point where the investment becomes worth it, but that cannot be known beforehand. I guess perhaps I’m trying to understand something that inherently cannot be understood, but I do wish there were some codified criteria by which we could make investment decisions on disruptive technologies. It seems any one disruptive technology could be the single technology that makes investors millions, but knowing the particular technology that will be a success is very difficult. This is fine for enterprise level business investment where big companies can diversify their portfolio and make 10 investments, but it doesn’t make sense for individual investors since the risk of failure is disaster.

Another thought I had while reading was in regard to the statement “Markets that do not exist cannot be analyzed.” I have heard many people (James Dyson included) say that market research is bollocks. Basically, don’t even waste your time doing market research because it’s just not worth the time or money. I see now why, and we should clarify – Don’t do market research on disruptive technologies – because it simply can’t be done. Any numbers you get are worthless. On the other hand, within sustaining technology space you should absolutely be doing market research. The market is well-defined and their needs can be analyzed.

I also like the idea of the Four Phases of Buying Hierarchy: functionality, reliability, convenience, and price. Basically this is what it means: Customers make buying choices based on how developed a technology is, and most technologies will progress through these four hierarchies. First, buyers are looking for functionality because there is nothing else out there. Once two products meet the functional needs, buyers will choose between the two by which one is more reliable. After that buyers make a choice based on which one is most convenient or easily accessible. Finally, in mature product markets customers will choose based on the lowest price. This is a very useful idea when dealing with what I do – product design. These four frameworks provide a reasonable guide for what to focus on during a design phase. Each buying hierarchy has it’s own specialized needs, and if you use the wrong one then you’re screwed. For example, HP’s failed Kittyhawk drive was designed within the “price” hierarchy with production capacity planned for thousands of units that were never realized. If they realized they were not in the “price” hierarchy, but instead in the “functionality” hierarchy they probably would have succeeded. Here are a few things to focus on for each hierarchy:

| Functionality | Focus on finding a market, and speed to market without much concern for bugs as these will get worked out later. |

| Reliability | Perform HALT/HASS/DVT/FMEA type tests to find failure points and design them out. |

| Convenience | Work on widening and simplifying the distribution networks. Hire UI/UX professionals to simplify your product. |

| Price | Focus on the Bill of Materials and the cost of every single item, how can you reduce it? |

I have put these phases into the process that Ransford Engineering uses for product design.

Introduction

In the cases of well-managed firms, good management was the most powerful reason they failed to stay atop their industries. Precisely because these firms listened to their customers, invested aggressively in new technologies that would provide their customers more and better products of the sort they wanted, and because they carefully studied market trends and systematically allocated investment capital to innovations that promised the best returns, they lost their positions of leadership.

Improved product performance – I call these sustaining technologies.

Occasionally, however, disruptive technologies emerge: innovations that result in worse product performance, at least in the near-term. Ironically, in each of the instances studied in this book, it was disruptive technology that precipitated the leading firms’ failure.

There are many examples in addition to the personal desktop computer and discount retailing examples cited above. Small off-road motorcycles introduced in North America and Europe by Honda, Kawasaki, and Yamaha were disruptive technologies relative to the powerful, over-the-road motorcycles made by Harley Davidson and BMW. Transistors were disruptive technologies relative to vacuum tubes. Health maintenance organizations were disruptive technologies to conventional health insurers.

Investing aggressively in disruptive technologies is not a rational financial decision. Disruptive products are simpler and cheaper; they generally promise lower margins, not greater profits. First commercialized in emerging or insignificant markets. Most profitable customers don’t want, and indeed initially can’t use, products based on disruptive technologies.

Only those companies that carefully measure trends in how their mainstream customers use their products can catch the points at which the basis of competition will change in the markets they serve.

Part 1: Why Great Companies Fail

Chapter 1: How Can Great Firms Fail? Insights from the Hard Disk Drive Industry

This is one of the innovator’s dilemmas: Blindly following the maxim that good managers should keep close to their customers can sometimes be a fatal mistake.

Chapter 2: Value Networks and the Impetus to Innovate

Henderson and Clark conclude that companies organizational structures typically facilitate component-level innovations, because most product development organizations consist of subgroups that correspond to a product’s components.

The organization’s structure and the way its groups lean to work together can affect the way it can and cannot design new products.

Tushman, Anderson, and their associates found that firms failed when a technological change destroyed the value of competencies previously cultivated and succeeded when new technologies enhanced them.

The disk drive industry displays a series of anomalies accounted for by neither set of theories.

Value Network – the context within which a firm identifies and responds to customers’ needs, solves problems, procures input, reacts to competitors, and strives for profit.

The way value is measured differs across networks.

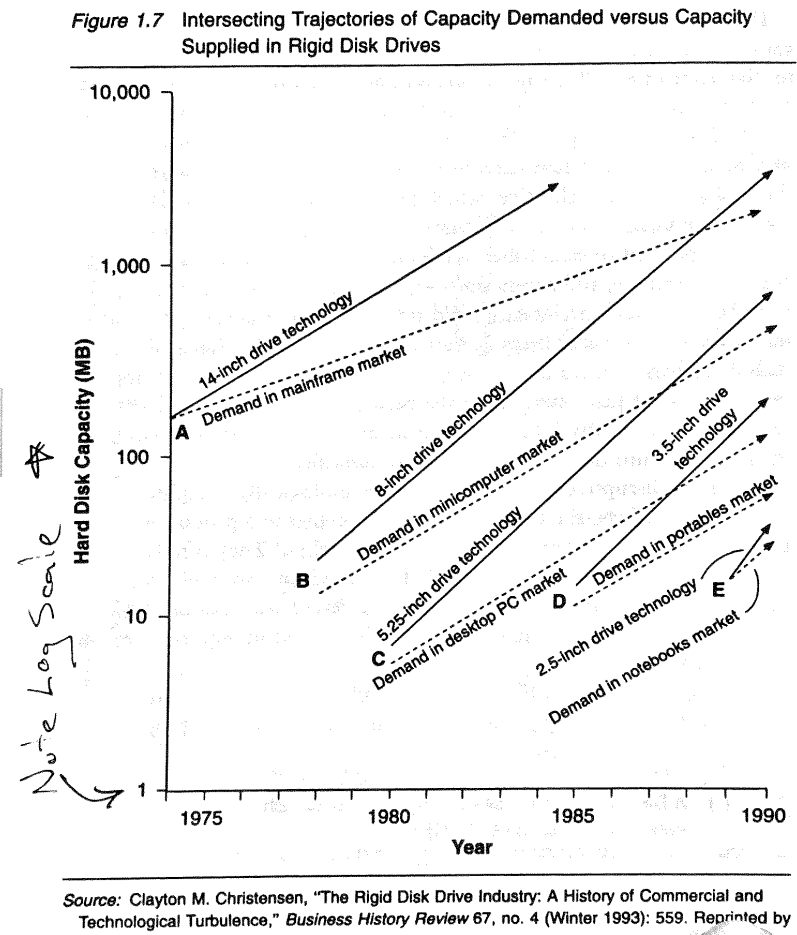

In the top-most value network, disk drive performance is measured in terms of capacity, speed, and reliability, whereas in the portable computing value network, the important performance attributes are ruggedness, low power consumption, and small size.

As firms gain experience within a given network, they are likely to develop capabilities, organizational structures, and cultures tailored to their value network’s distinctive requirements My note: naturally blocking themselves out of other value networks.

Makers of mainframe computers historically needed gross profit margins of between 50% and 60% to cover the overhead cost structure inherent to the value network in which they competed. The portable computer value network, however, can be profitable with gross margins of 15 to 20%.

The technology S-curve forms the centerpiece of thinking about technology strategy. It suggests that the magnitude of a product’s performance improvement in a given time period or due to a given amount of engineering effort is likely to differ as technologies mature. The theory posits that in the early stages of a technology, the rate of progress in performance will be relatively slow. As the technology becomes better understood, controlled, and diffused, the rate of technological improvements will accelerate. But in its mature stages, the technology will asymptotically approach a natural or physical limit such that ever greater periods of time or inputs of engineering effort will be required to achieve improvements.

The typical management decision-making process:

Step 1: Disruptive Technologies Were Developed within Established Firms

Engineers at Seagate Technology made some eighty prototype models before the issue of formal project approval was raised with senior management.

Step 2: Marketing Personnel Then Sought Reactions from Their Lead Customers with negative reactions

Step 3: Established Firms Set Up the Pace of Sustaining Technological Development

Sustaining investments appeared far less risky than investments in the disruptive technology: the customers existed, and their needs were known.

Step 4: New Companies Were Formed, and Markets for the Disruptive Technologies Were Found by Trial and Error

New companies, usually including frustrated engineers from established firms, were formed to exploit the disruptive product architecture.

Step 5: The Entrants Moved Upmarket

Step 6: Established Firms Belatedly Jumped on the Bandwagon to Defend Their Customer Base

Chapter 3: Disruptive Technological Change in the Mechanical Excavator Industry

Four of the thirty or so established manufacturers of cable-actuated equipment in the business in the 1950s had successfully transformed themselves into sustainable hydraulic excavator manufacturers by the 1970s.

Because [early hydraulic excavator’s] capacity was so small and their reach so short, they were no use to mining, general excavation, or sewer contractors, who were demanding machines with buckets that held 1 to 4 cubic yards. As a result, the entrant firms had to develop a new application for their products. Disruptive technologies need to be sold to anyone that will buy.

This is typical of industries facing a disruptive technology: The leading firms in the established technology remain financially strong until the disruptive technology is, in the midst of their mainstream market.

Consistently, established firms attempt to push the technology into their established markets, while the successful entrants find a new market that values the technology.

Chapter 4: What Goes Up, Can’t Go Down

Rational managers can rarely build a cogent case for entering small, poorly defined low-end markets that offer only lower profitability.

Part 2: Managing Disruptive Technological Change

Five fundamental principles of organizational nature that managers in the successful firms consistently recognized and harnessed.

- Resource dependence: Customers effectively control the patterns of resource allocation in well-run companies.

- Small markets don’t solve growth needs of large companies.

- The ultimate uses or applications for disruptive technologies are unknowable in advance. Failure is an intrinsic step toward success.

- Organizations have capabilities that exist independently of the capabilities of the people who work within them. Organizations’ capabilities reside in their processes and their values – and the very processes and values that constitute their core capabilities within the current business model also define their disabilities when confronted with disruption.

- Technology supply may not equal market demand. The attributes that make disruptive technologies unattractive in established markets often are the very ones that constitute their greatest value in emerging markets.

How did the successful managers harness these principles to their advantage?

- They embedded projects to develop and commercialize disruptive technologies within an organization whose customers needed them. When managers aligned a disruptive innovation with the “right” customers, customer demand increased the probability that the innovation would get the resources it needed.

- They placed projects to develop disruptive technologies in organizations small enough to get excited about small opportunities and small wins.

- They planned to fail early and inexpensively in the search for the market for a disruptive technology. They found that their markets generally coalesced through an iterative process of trial, learning, and trial again.

- They utilized some of the resources of the mainstream organization to address the disruption, but they were careful not to leverage its processes and values. They created different ways of working within an organization whose values and cost structure were turned to the disruptive task at hand.

- When commercializing disruptive technologies, they found or developed new markets that valued the attributes of the disruptive products, rather than search for a technological breakthrough so that the disruptive product could compete as a sustaining technology in mainstream markets.

Chapter 5: Give Responsibility for Disruptive Technologies to Organizations Whose Customers Need Them

In practice, it is a company’s customers who effectively control what it can and cannot do.

Clearly, customers wield enormous power in directing a firm’s investments. What should managers do when faced with a disruptive technology that the company’s customers explicitly do not want? One option is to convince everyone in the firm that the company should pursue it anyway, that it has long-term strategic importance despite rejection by the customers who pay the bills and despite lower profitability than the upmarket alternative. The other option would be to create an independent organization and embed it among emerging customers that do need the technology. ….. The second option offers the higher probabilities of success than the first.

Yet IBM’s success in the first five years of the personal computing industry stands in stark contrast to the failure of the other leading mainframe and minicomputer makers to catch the disruptive desktop computing wave. How did IBM do it? It created an autonomous organization in Florida, far away from its New York state headquarters.

Traditional department stores historically marked merchandise up by 40 percent and turned their inventory over four times a year – that is, they earned 40 percent on the amount they invested in inventory, four times during the year, for a total return on inventory investment of 160 percent.

| Retailer Type | Gross Margins | Inventory Turns per Year | Returns on Inventory |

| Department Stores | 40% | 4x | 160% |

| Discount Retailers | 20% | 8x | 160% |

Establishing independent organizations to pursue disruptive technology seems to be a necessary condition for success.

Two models for how to make money cannot peacefully coexist within a single organization.

Chapter 6: Match the Size of the Organization to the Size of the Market

Creating new markets is significantly less risky and more rewarding than entering established markets against entrenched competition.

There is no evidence that the leaders [in a particular technology] gained any significant competitive advantage over the followers; none of the firms that pioneered thin-film technology gained significant market share on that account.

It is, indeed, an innovator’s dilemma. Firms that sought growth by entering small, emerging markets logged twenty times the revenues of the firms pursuing growth in larger markets.

Rising share prices make stock option plans an inexpensive way to provide incentive to and to reward valuable employees.

How can a manager of a large, successful company deal with these realities of size and growth when confronted by disruptive change? I have observed three approaches in my study of this problem:

- Try to affect the growth rate of the emerging market, so that it becomes big enough, fast enough, to make a meaningful dent on the trajectory of profit and revenue growth of a large company.

- Wait until the market has emerged and become better defined and then enter after it “has become large enough to be interesting.”

- Place responsibility to commercialize disruptive technologies in organizations small enough that their performance will be meaningfully affected by the revenues, profits, and small orders flowing from the disruptive business in its earliest years.

The Apple II sold 43,000 computers in the first two years 1977-1978. Apple sold 140,000 Newton personal digital assistants (PDAs) in 1993 and 1994, but most observers viewed the Newton as a big flop. …. It outsold the Apple II in its first two years by a factor of more than three to one. But while selling 43,000 units was viewed as an IPO-qualifying triumph in the smaller Apple of 1979, selling 140,000 Newtons was viewed as a failure in the giant Apple of 1994.

In launching the Newton, however, Apple was desperate to short-circuit this coalescent process for defining the ultimate product and market. It assumed that its customers knew what they wanted and spent very aggressively to find out what this was.

Large companies should seek to embed the project in an organization that is small enough to be motivated by the opportunity offered by a disruptive technology in its early years. This can be done either by spinning out an independent organization or by acquiring an appropriately small company.

Chapter summary: It is not crucial for managers pursuing growth and competitive advantage to be leaders in every element of their businesses. In sustaining technologies, in fact, evidence strongly suggests that companies which focus on extending the performance of conventional technologies, and choose to be followers in adopting new ones, can remain strong and competitive. This is not the case with disruptive technologies, however. There are enormous returns and significant first-mover advantages associated with early entry into the emerging markets in which disruptive technologies are initially used. Disk drive manufacturers that led in commercializing disruptive technology grew at vastly greater rates than did companies that were disruptive technology followers.

Chapter 7: Discovering New and Emerging Markets

Markets that do not exist cannot be analyzed.

My Notes: Expect your estimates of sales and volume to be off by an order of magnitude in either direction. Feel, explore your way into emerging markets, don’t assume you know the needs and the market size.

Intel’s system for allocating production capacity operated according to a formula whereby capacity was committed in proportion to the gross margins earned by each product line. The system therefore imperceptibly began diverting investment capital and manufacturing capacity away from the DRAM business and into microprocessor – without an explicit management decision to do so.

Amid all the uncertainty surrounding disruptive technologies, managers can always count on one anchor: Expert’s forecasts will always be wrong.

Believing they had identified the winning strategy, [HP’s Kittyhawk team] managers spent their budget on a product design and the manufacturing capacity for a market application that never emerged. When the ultimate applications for the tiny drive ultimately began to coalesce, the Kittyhawk team had no resources left to pursue them.

Plans to Learn versus Plans to Execute: In general, for sustaining technologies, plans must be made before action is taken, forecasts can be accurate, and customer inputs can be reasonably reliable. Careful planning, followed by aggressive execution, is the right formula for success in sustaining technology.

I have come to call this approach to discovering the emerging markets for disruptive technologies agnostic marketing, by which I mean marketing under an explicit assumption that no one – not us, not our customers – can know whether, how, or in what quantities a disruptive product can or will be used before they have experience using it.

Note 8. Studies of how managers define and perceive risk can significant light on this puzzle. Amos Tversky and Daniel Kahneman, for example, have shown that people then to regard propositions that they do not understand as more risky, regardless of their intrinsic risk, and to regard things they do understand as less risky, again without regard to intrinsic risk. Managers, therefore, may view creation of new markets as risky propositions, in the face of contrary evidence, because they do not understand non-existent markets; similarly, they may regard investment in sustaining technologies, even those with high intrinsic risk, as safe because they understand the market need.

Chapter 8: How to Appraise Your Organization’s Capabilities and Disabilities

Three classes of factors affect what an organization can and cannot do: its resources, its processes, and its values.

Resources include people, equipment, technology, product designs, brands, information, cash, and relationships with suppliers, distributors, and customers. Resources are usually things or assets – they can be hired and fired, bought and sold, depreciated or enhanced.

The patterns of interaction, coordination, communication, and decision-making through which they accomplish transformations are processes. Processes include not just manufacturing processes, but those by which product development, procurement, market research, budgeting, planning, employee development and compensation, and resource allocation are accomplished.

Some of the most crucial processes to examine as capabilities or disabilities aren’t the obvious value-added processes involved in logistics, development, manufacturing, and customer service. Rather, they are the enabling or background processes that support investment decision-making.

The values of an organization are the criteria by which decisions about priorities are made.

An organization’s values are the standards by which employees make prioritization decisions – by which they judge whether an order is attractive or unattractive; whether a customer is more important or less important; whether an idea for a new product is attractive or marginal; and so on. Prioritization decisions are made by employees at every level.

A key metric of good management, in fact, is whether such clear and consistent values have permeated the organization.

One reason that many soaring young companies flame out after they go public based upon a hot initial product is that whereas their initial success was grounded in resources – the founding group of engineers – they fail to create processes that can create a sequence of hot products.

If a manager determined that an employee was incapable of succeeding at a task, he or she would either find someone else to do the job or carefully train the employee to be able to succeed. Training often works, because individuals can become skilled at multiple tasks. Despite beliefs spawned by popular change-management and reengineering programs, processes are not nearly as flexible or “trainable” as resources – and values are even less so. The processes that make an organization good at outsourcing components cannot simultaneously make it good at developing and manufacturing components in-house. Values that focus an organization’s priorities on high-margin products cannot simultaneously focus priorities on low-margin products. This is why focused organizations perform so much better than unfocused ones: their processes and values are matched carefully with the set of tasks that need to be done. For these reasons, managers who determine that an organization’s capabilities aren’t suited for a new task, are faced with three options through which to create new capabilities. They can:

- Acquire a different organization whose processes and values are a close match with the new task.

- Try to change the processes and values of the current organization.

- Separate out an independent organization and develop within it the new processes and values that are required to solve the new problem.

Proccesses and values are by their very nature inflexible.

When disruptive change appears on the horizon, managers need to assemble the capabilities to confront the change before it has affected the mainstream business.

It is impossible to ask one process to do two fundamentally different things. The market research and planning processes that are appropriate for the launch of new products into existing markets simply aren’t capable of guiding a company into emerging, poorly defined markets.

Chapter 9: Performance Provided, Market Demand, and the Product Life Cycle

Rates of product performance improvement have exceeded the rates that the market has needed or was able to absorb.

My thoughts: How can you tell when this is happening and pull back on development?

Performance oversupply is an important factor driving the transition from one phase of the cycle to the next. The product evolution model, called the buying hierarchy by its creators, Windmere Associates of San Francisco. Four phases of buying hierarchy: functionality, reliability, convenience, and price. Initially, when no available product satisfies the functionality requirements the market, the basis of competition, or the criteria by which product choice is made, tends to be product functionality. (Sometimes a market may cycle through several different functionality dimensions.) Once two or more products credibly satisfy the market’s demand for functionality, however, customers can no longer base their choice of products on functionality, but tend to choose a product and vendor based on reliability. As long as market demand for reliability exceed what vendors are able to provide, customers choose products on this basis – and the most reliable vendors of the most reliable products earn a premium for it.

But when two or more vendors improve to the point that they more than satisfy the reliability demanded by the market, the basis of competition shifts to convenience. Customers will prefer those products that are the most convenient to use and those vendors that are most convenient to deal with. Again, as long as the market demands for convenience exceeds what vendors are able to provide, customers choose products on this basis and reward vendors with premium prices for the convenience they offer. Finally, when multiple vendors offer a package of convenient products and services that fully satisfies market demand, the basis of competition shifts to price. The factor driving the transition from one phase of the buying hierarchy to the next is performance oversupply.

Other Consistent Characteristics of Disruptive Technologies

Managers must understand that these characteristics to effectively chart their own strategies for designing, building, and selling disruptive products.

1. The Weakness of Disruptive Technologies Are Their Strengths

The firms that were most successful in commercializing a disruptive technology were those framing their primary development challenge as a marketing one: to build or find a market where product competition occurred along dimensions that favored the disruptive attributes of the product.

2. Disruptive Technologies Are Typically Simpler, Cheaper, and More Reliable and Convenient than Established Technologies

Three strategic alternatives for disruptive technologies that will change the nature of competition:

- Most common. Ascend the trajectory of sustaining technologies into ever-higher tiers of the market, ultimately abandoning lower-tier customers when simpler, more convenient, or less costly disruptive approaches emerge.

- Difficult to do. March lock-step with the needs of customers in a given tier of the market, catching successive waves of change in the basis of competition.

- Use marketing initiatives to steepen the slopes of the market trajectories so that customers demand the performance improvements that the technologies provide. (For example, Microsoft marketed software packages that consumed massive amounts of disk memory and required faster processors.)

Which of the strategies illustrated is best? This study finds clear evidence that there is no one best strategy.

Chapter 10: Managing Disruptive Technological Change: A Case Study

Christiansen discusses electric vehicles, I took no notes.

Chapter 11: The Dilemmas of Innovation: A Summary

No notes.